How quickly things can change

Since the depths of the market declines in mid-March, when liquidity in equity and credit markets around the world caused panic in markets, we have seen a dramatic rebound. How quickly things can change.

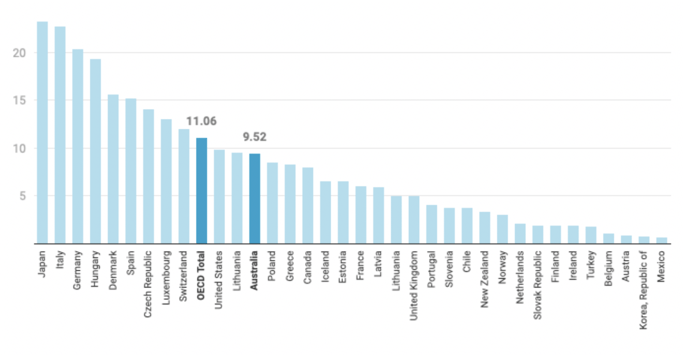

The stabilisation and turnaround of markets was led by a massive co-ordinated stimulus program globally and the belief that countries around the world were starting to “flatten the curve” in relation to COVID-19. The announcement by the US government on Sunday March 22nd of a $2 trillion stimulus package and a $2 trillion bond buying program by the US Fed. Australia also followed suit announcing stimulus which totals 9.5% of GDP and is one of the highest in the world.

COVID-19 fiscal stimulus as % of GDP, OECD nations.

The result of this stimulus was a rebound the US S&P 500 of 29% since the bottom of March 23 and the ASX300 of 17%. A simply astounding turnaround given that the impact to the global economy and company earnings still remains extremely uncertain.

On Monday April 20, we saw another historical event, with oil prices dropping into negative territory. This was in response to oil producers not cutting supply of oil by anywhere near the amount to offset the fall in demand for oil globally. This led to a massive oversupply which filled every available storage facility or tanker, which rendered the price of oil essentially worthless.

It is important to remember that just as markets have fallen c30-35% in record time since the COVID-19 pandemic took hold, and subsequently bounced 25-30% in further record time on the announcement of stimulus programs; it is entyrely possible that markets will remain volatile and more bad news regarding COVID-19, economic growth or corporate earnings could see markets fall again.

As investment managers, our role is to look through this uncertainty and continue with our long-term strategic investment programs. The objective being to maintain the risk-return profiles of our funds for the long-term benefit of our members. We continue to closely monitor and rebalance our portfolios.

The Crescent Wealth portfolios are inherently conservative due to our views on the previous extremes of market valuations and our high holdings in Islamic Cash. The cash holdings of the Conservative option, Balanced option and Growth option all remain high and have positioned the funds well for a market sell off.

It is important to remember that superannuation is a very long-term investment for the vast majority for Crescent Wealth’s members. While markets are currently extremely volatile, we remain vigilant in monitoring the situation and managing the portfolio closely.

Share this

End of year 2023 investment update

Australian Federal Budget Superannuation Update