Australian listed real estate securities have been a major investment pathway for investors seeking stable dividend income and the prospect of moderate capital appreciation. As global demographics shift and the world dives further into the information age, real estate in Australia has been relatively slow to present adequate exposure to asset classes that benefit from this transition.

Whilst Australia is deservedly known for having some of the highest quality real estate companies with highly experienced management, investors in listed equities are often forced to choose between traditional asset classes such as retail in the form of Scentre Group (Westfield assets in Australia), office, and a single large industrial owner and developer (Goodman Group). Global real estate is a keyway investors can gain exposure to asset classes which benefit from large structural trends such as an ever increasing need for data storage and data transfer, an ageing population across the developed world and the inroads e-commerce is making into physical retail.

Listed Real Estate in Australia

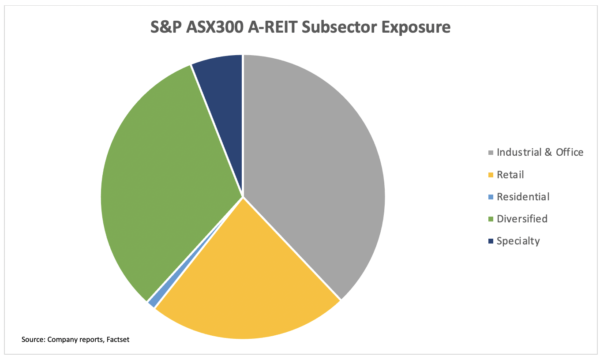

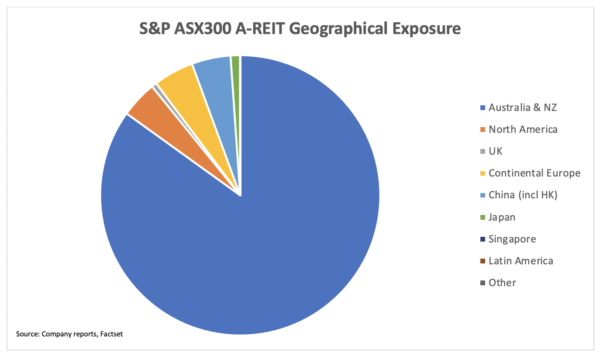

The S&P ASX A-REIT indices are the most followed ASX listed real estate benchmarks. S&P track two separate A-REIT indices consisting of ASX200 and ASX300 securities. The S&P ASX200 A-REIT Index tracks 20 of the largest and most liquid real estate companies listed in Australia, whilst the S&P ASX 300 A-REIT Index adds an additional 10 mid/small cap names. Thus, for Australian investors seeking listed property, the universe of stocks to filter through is around 30 securities. As we will show, this introduces a certain level of concentration risk both at the security, subsector and geographical level.

For instance, as at October 2020, the S&P ASX 300 A-REIT Index, the more diversified index has a >25% exposure to a single company, Goodman Group. Furthermore, >92% of the index is invested in traditional real estate such as retail, office or industrial and ~84% of assets by value are located in Australia or New Zealand.

A Global Alternative

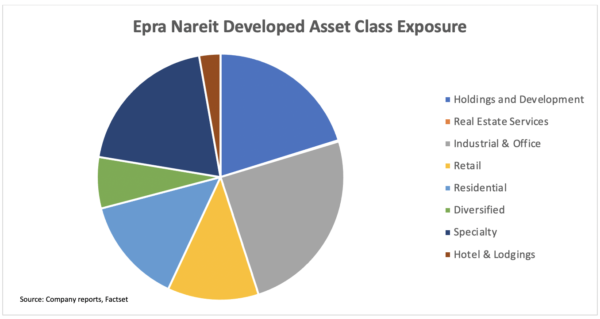

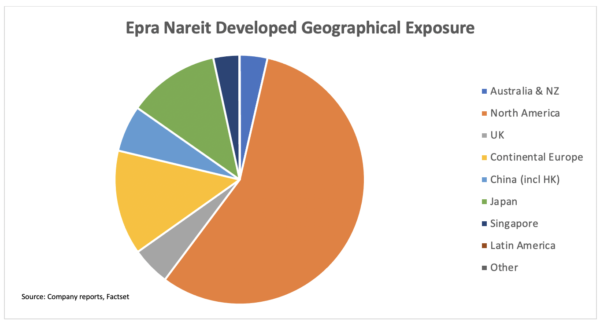

Recognising the concentration risk present in Australian real estate, a global approach may present a compelling option. The EPRA Nareit Developed Index is a prime example of a highly diversified real estate index with lower concentration risk at the stock, subsector and geographical level. As a starting point with 342 constituents, its largest position makes up ~5% of the index weight. Subsector exposures are also more diversified with a 20% weighting to specialised REITs, a 14% exposure to pure-play residential and a 3% exposure to hotels. Many of these subsectors within the specialised category include; Data Centres, Communication Towers, Hospitals and Clinics are not available to Australian REIT investors. However, geographical concentration remains a sizeable risk with US listed real estate dominating most global indices with >50% allocations.

Key Subsectors

The benefits from diversifying into global real estate will also come in the form of exposure in new real estate subsectors with structural tailwinds not yet available on the ASX:

- Data Centres

- Communication Towers

Data Centres

At a fundamental level, data centre REITs provide space to accommodate electrical and thermal equipment to house servers and networking equipment. To generate rental and other income streams data centre owners will lease out space (racks) with power and connectivity (to other data sources). Tenants will often, but not always own and manage the equipment housed in the data centre. Companies will opt to use a data centre as it requires lower set up costs or a lower risk of catastrophe risk as data centres offer near 100% online capability with multiple risk mitigation tools such as armed security, backup generators and natural disaster proof locations. The growth in data traffic accelerated by mobile penetration, video on demand services and cloud computing has seen demand for data infrastructure grow at unprecedented levels. With major data centre owners largely presiding in the US, global real estate is a key way to gain exposure to global data traffic growth.

Communication Towers

Simply put, communication tower REITs lease space in key locations to communication providers so their customers are able to access wireless telecommunication and data services. As consumers demand better coverage and faster speeds, towers and small cells will need to be in more locations with higher specifications. The advent of 5G will also naturally require a higher density network as the higher frequency signal has physical limitations travelling large distances. Communication towers are an investment opportunity not currently available in Australia but are a mainstay of the US REIT sector and Indonesia Stock Index.

Conclusion

A wider range of alternative subsectors in high growth areas await investors willing to look outside of the ASX listed real estate. Data centres and communication towers are and will continue to be staple infrastructure in the information age, neither of which are available to A-REIT investors currently. Outside of growth subsectors, geographical diversity and a lower stock concentration risk are key differentiators for investors able to look globally.

The ASX listed property fund managers and Australian real estate investment trusts such as GPT, Dexus, Mirvac, Charter Hall and Stockland would benefit from expanding their diversified portfolio across not only residential property, commercial property, shopping centres and sectors such as healthcare but also into asset classes that are aligned with the growth of data-centred operations.

The need to balance capital gain returns, rental incomes, gearing and liquidity in order to ensure future performance is equivalent to or better than past performance lies at the core of the A-REIT sector and there are longer term gains to the achieved in this low-interest rate environment.

Share this

Spotlight on ethical investments – Healthcare

Australia’s water market: Investing in a sustainable future