Investing in Data Centre Primer

Data centres assist businesses by allowing them to outsource computing power and/or digital data storage.

Data centres are generally classifieds in one of the following categories:

- Colocation (or carrier-neutral) Colocation data centres provide equipment, space and bandwidth to customers and enable interconnection with other tenants, cloud providers and telecommunication providers. Tenants at the data centres are able to use multiple carriers to connect cloud/IT infrastructure and critical systems to the internet, eliminating the risk of downtime, and have flexibility in switching carriers due to price and routing service without having to move servers to another location. These data centres can also provide private networks between the company’s operations and Colocation providers include NextDC, Equinix, Digital Realty, Global Switch and AirTrunk. Colocation facilities can further be classified as either retail data centres, which offer services to enterprises, or wholesale data centres, which offer services to large enterprises and hyperscalers, or a combination of both. Data centre REITs typically sell co-location services.

- Telecom (or carrier) Telecom data centres are operated by telcos or internet service providers who cross-sell data services to their existing customers. They may offer managed hosting and value-added services, although the choice of network service provider is often limited to the carrier operating the data centre. Telecom data centre providers in Australia include Telstra, Vocus and TPG.

- Hyperscaler (or cloud provider) Major hyperscale companies may host their cloud servers in their own data centres and provide tenants with hardware, software and system integration These data centres may be carrier specific, although are typically carrier-neutral. Hyperscale providers include AWS, Google, Microsoft and Alibaba.

What do Data Centres do and how do they earn revenue?

Data centre REITs typically build centres in key network locations, provide infrastructure for drawing power and cooling, then lease space or “racks” to customers wanting a reliable location to store and use their information infrastructure. Customers will pay a recurring fee for the rack and pay for their own power use, power usage is typically a pass-through cost for the Data Centre REIT.

Another key increasingly important revenue driver for data centres is the ability to charge tenants for interconnection. Interconnection in its simplest form is to connect two different customers within the data centre infrastructure whether the connection is physical or a software solution. This allows the two tenants to access each other’s servers without using a “public” connection such as a telecommunication provider allowing for faster and more reliable connection. Data Centres will charge an on-going interconnection fee for this. The importance of scale is highlighted in interconnection as larger data centres are able to interconnect more tenants globally.

Generally, the more developed a data centre market is, the more interconnection revenue is derived from it.

Capital costs to build data centres are high further highlighting the importance of scale. Unlike another commercial real estate where the land is the largest cost, land typically comprises just 5-10% of the total build cost of a data centre. Fitouts, electrical systems, air conditioning play a much larger role in the cost structure of a build.

Barriers to entry is also high with certification of uptime a key requirement to attract tenants. Data centres are expected to run without failure and very little maintenance. The Uptime Institute is the global standard for grading data cente uptimes, their requirements are as follows:

- Tier 1 – 99.671% uptime or 28.8 hours of downtime per year

- Tier 2 – 99.741% uptime or 22.7 hours of downtime per year

- Tier 3 – 99.982% uptime or 1.6 hours of downtime per year with 72 hours of outage protection

- Tier 4 – 99.995% uptime 28 minutes of downtime per year with 96hours of outage protection

Tenant Profiles

Customers can generally be broken into two types, wholesale and retail.

Wholesale tenants generate fewer sales per unit of capacity, require larger power output, but will generally have long lease terms and are an important selling point to all other customers. Customers such as Amazon Web Services (AWS) Microsoft (Azure), Google Cloud also interconnect with other tenants ensuring low latency for all tenants. Although not a perfect analogy, large wholesale customers can be seen as the anchor tenants which drive other data traffic as an anchor supermarket would in a shopping centre.

Retail customers such as small to medium enterprises, startups generate better unit economics and require less power but have shorter terms and are considered a lower quality credit.

Industry Trends

As one would expect, the growth of data centre revenue is directly related to the amount of data that needs to be stored and accessed globally. Colocation services is expected to grow at mid to high single digits, whilst interconnection revenue is expected to grow at low double digits CAGR in the medium term.

Short Company Profiles

The fund is invested in Digital Realty, and Coresite Realty. Equinix does not pass Shariah compliance.

Equinix (EQIX)

EQIX is the world’s largest Data Centre company with a portfolio of 22 data centres across 26 countries. Equinix is well-diversified by tenant industry, services and geography with its largest tenants accounting for less than 3% of total revenues.

Digital Realty (DLR)

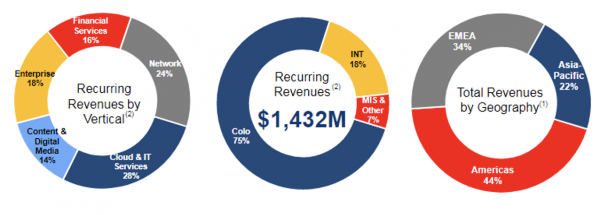

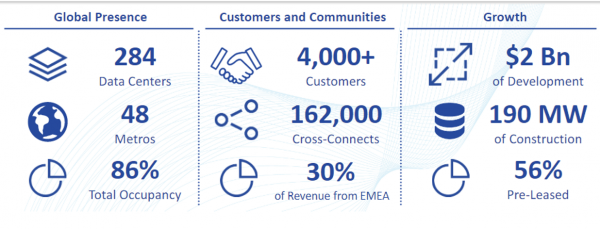

DLR is the second-largest Data Centre provider by market capitalisation. With 284 data centres globally and a majority skew to North America and Europe, DLR is well diversified by location and tenant group.

CoreSite Realty (COR)

CoreRealty is a US pure-play data centre developer and operator. It operates 23 data centres primarily in Los Angeles, Denver, San Francisco, New York, Boston, Chicago and Miami. In its earlier stage of development, COR is able to develop meaningful projects to enhance its portfolio quality and grow earnings.

The Risks

Data Centres are becoming more relevant and important in a deeply digitally penetrated world, however they are not immune to risks such as:

- Development risks – With the majority of data centres being built as greenfield or brownfield projects, site acquisition and development projects are necessary to increase capacity, where sites are scarce and developments are built with little pre-leasing there is risk that companies take excess development risk.

- Competitive environment – in a structurally growing industry, players are either competing for market share, or are at risk of falling behind the competition. Subscale players with little development capability are at most risk to become irrelevant or will be acquired by larger players.

- Power of tenants – As the tenants of the data centres get larger and more entrenched as cloud service providers, the power balance could continue to shift towards the like of Amazon, Microsoft and Google leading to discounting of prices or internalisation of data centre services.

Conclusion

Data centres are a key infrastructure enabler of the information technology age. It is an attractive industry with structural tailwinds as data usage, access and storage continue to grow. Data Centre REITs are an attractive way to gain exposure to this thematic with solid economics. As the market grows organically at 5-10%, additional services such as interconnection will serve as high margin incremental income with relatively low current penetration.

Share this

How Do Islamic Investors Earn Interest Under Sharia Law?

How to Invest Halal In Australia