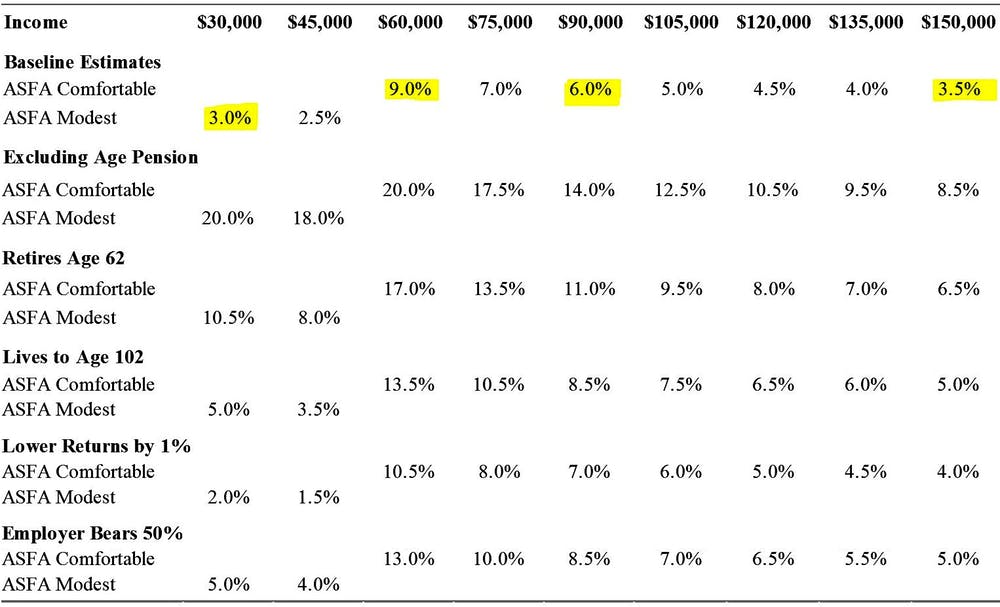

A team of researchers from the Australian National University set out to reveal the uncomfortable truth about super: that there’s no one-size-fits-all solution for contributions. It’s all dependant on your lifestyle, your risk appetite and what you want to accomplish with your investments.

They put into practice a ‘stochastic life-cycle model’ to “calculate the optimal level of super contributions for Australians at nine different income levels (ranging from AU$30,000 to $150,000), applying existing tax, super and pension rules.”

The result? An accurate table of estimates that reveals some optimal super contributions by income level and objectives:

Of course, these figures won’t remain static for everyone. You might decide to do nothing about a compulsory contribution rate that’s set too high for your desires, while alternatively you might choose to add more contributions if the rate is too low for your aspirations.

You can read the full explanation at SuperGuide here.

Staying with informative tips published by SuperGuide, they have a number of suggestions on how you can boost your retirement savings with a super contribution that is also tax-deductible – meaning you get the best of both worlds.

It’s important to remember that there are some rules and limits in place to ensure individuals don’t take advantage of this system more than they should. For example, you can’t claim any tax deductions on the standard super contributions from your employer (including the current 9.5% compulsory super guarantee).

You can find out more at SuperGuide.

Finally, if you’re thinking about downsizing your home and want to bolster your superannuation before retiring, there’s another government incentive you can take advantage of. Called the ‘downsizer contribution’, you can commit up to $300,000 from the sale of your property directly into your super, or up to $600,000 as a couple. Whether or not this strategy is right for you will depend on your lifestyle needs and your current circumstances, but it could be a handy way to boost your savings before you retire.

Share this

Febfast and why Crescent Wealth focuses on ethical investments for your long-term future

Snapshot of Influences on your Superannuation